》Check SMM copper quotes, data, and market analysis

》Click to view the historical price trend of SMM spot copper

SMM July 3rd News:

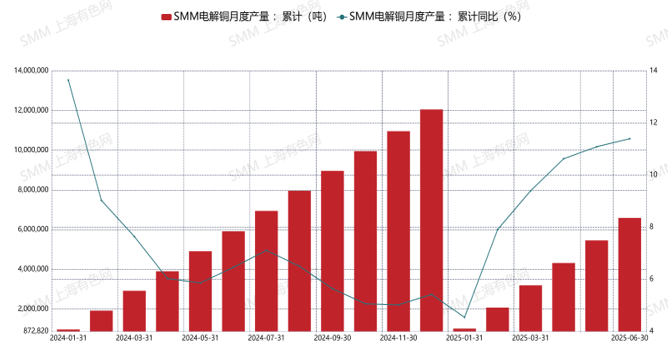

As the first half of 2025 has passed, domestic copper cathode production has reached a new high. According to SMM statistics, the cumulative production of copper cathode from January to June 2025 was 6.593 million mt, up 674,700 mt YoY, with a growth rate of 11.40%. For the specific trend, see the chart below:

So, how do domestic smelters ensure the supply of raw materials? We analyze the following reasons:

- Increase the supply of domestic ore. According to SMM statistics, the production of domestic ore in the first half of this year was 964,800 mt in metal content, up 126,000 mt YoY, with a growth rate of 15.02%;

- Increase the supply of imported ore. According to customs data, the imports of copper concentrates in the first half of this year were approximately 15.0123 million mt in physical terms, equivalent to 3.7831 million mt in metal content, up 277,700 mt in metal content YoY, with a growth rate of 7.92%. The increase in imports far exceeds that of overseas copper concentrates, forcing some overseas smelters to cut production.

3. Increase the procurement volume of copper anode. According to SMM statistics, since last year, enterprises producing anode plates from scrap have mushroomed nationwide. In contrast, the production of secondary copper rod enterprises has been declining. Specifically, the total production of secondary copper rod enterprises from January to June 2025 was 1.0438 million mt, down 80,400 mt MoM, with a decline rate of 7.15%. However, the production of anode plates from scrap in the first half of the year was 701,000 mt, up 132,000 mt MoM, with a growth rate of 23.20%. Nevertheless, the domestic production of anode plates from mines in the first half of this year was only 377,000 mt, down 33,000 mt YoY. The main reason for the decline in production is that some anode plate enterprises have extended their industry chains to produce copper cathode.

4. However, the imports of anode plates have been declining. According to customs data, the imports of anode plates in the first half of this year were approximately 386,200 mt, down 74,300 mt YoY, with a decline rate of 16.8%. The reasons for such a significant decline are as follows: First, overseas demand for anode plates has increased; second, some anode plates have been imported as red copper ingots. According to customs data, the imports of red copper ingots from January to June 2025 were approximately 232,000 mt, up 124,500 mt YoY, with a growth rate of 116%.

5. Affected by the fact that the price difference between copper cathode and copper scrap was not as good as that in the first half of last year, the direct use of copper scrap for cold materials was only 158,000 mt from January to June 2025, down 27,000 mt compared to 185,000 mt in the same period last year.

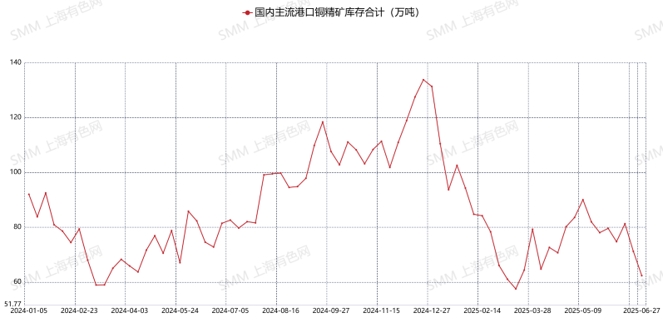

- Consumption of copper concentrate inventory at ports. According to SMM statistics, as of June 27, 2025, the total inventory of copper concentrates at domestic mainstream ports was 623,500 mt in physical terms, down 190,800 mt compared to 814,300 mt in the same period last year, equivalent to approximately 48,000 mt in metal content, with a decline rate of 23.43%.

In summary, the combined increase in the aforementioned raw materials (domestic copper concentrates, imported copper concentrates, domestic copper anodes, imported copper anodes, copper scrap, and port inventories) from January to June 2025 was 573,900 mt. When considering the supplementary supply from other raw materials, we believe it is reasonable for copper smelters to achieve such a significant increase in H1. Looking ahead, there is still an expected capacity increase of over 1.3 million mt in domestic smelters in H2 of this year and next year. It will be a challenging task for domestic smelters to maintain such a rapid growth rate, requiring both internal and external efforts to achieve the goal.